2020-03-25 13:22:51

European Recycling Markets Reel from Coronavirus

2020-03-25 13:22:51

Concerns over the long-term impact of the coronavirus outbreak on key European recycling markets sharply escalated this week following the adoption of further containment measures across the continent.

Sources are particularly worried about limited volumes entering collection systems, logistic disruptions, potential downstream demand losses in non-packaging sectors, buyers abandoning sustainability measures and a reduction in necessary long-term investment.

Even at the end of last week, concerns in the recycling industry had only been limited to the impact on virgin prices—with which recycled material competes—and individual customer relationships in countries such as Italy.

The coronavirus has had a major impact on petrochemicals, hindering global supply chains, changing consumer demand patterns and prompting wide swings in the markets. At the same time, crude has plunged in the wake of the ongoing price war between Saudi Arabia and Russia—which is also being felt in virgin plastics markets across Europe.

In the meantime, the recycling markets have largely been trading normally, albeit with some additional buyer caution. This, however, is beginning to shift.

Changes in Consumer Behavior

Sources in the recycled polyethylene terephthalate (R-PET) market—the most widely recycled plastic across Europe—are already seeing a change in consumer behavior, particularly around buying habits, and more importantly, recycling habits.

“People are buying [bottled] water and they don't bring it back, they store it,” a German recycler said on Tuesday. Demand for virgin PET has already increased significantly in March as Europeans began to panic buy food and other necessities.

“On the one hand, it's a regular seasonal effect in February and March – it’s winter so people drink less [bottled drinks]. But on the other, purchasing has increased big time, so [consumers] store [bottles] at home, [and] some have switched to glass,” the recycler added.

Sources in Germany, which has one of the most established deposit return schemes (DRS) in Europe – where consumers return their used PET bottles via reverse vending machines in locations like supermarkets – are waiting to assess the impact of social distancing and self-isolation on the recycling market.

Many will be looking at how used PET bottles are returned to the recycling stream during the outbreak as it comes at a time when post-consumer bottle availability is already tight due to the previously mentioned drop in bottled-drinks consumption.

This is also likely to have an effect on seasonal trends associated with the consumption of bottled drinks. If social distancing is still in effect during the summer, people may not go out as much, resulting in less R-PET availability. Some said the coronavirus may cause more people to turn to tap water or use glass bottles over plastic.

A similar trend of reduced collection rates is expected in other key recycled polymer sectors such as recycled polyethylene (R-PE) and recycled polypropylene (R-PP).

“We plan that we will have less material getting into our plants in the next weeks,” a major French waste collector and reprocessor said.

Reduced collection rates typically take several weeks to be felt in the market because of the time it takes post-consumer or post-industrial material to work through the chain. This means that any shortages most likely will be felt during what would typically be the beginning of the peak season for R-PET and recycled polyolefins (R-PO). Nevertheless, given the demand uncertainty it is unlikely that the 2020 peak season will be typical.

The impact on demand for R-PO is likely to be divided by end-use market. Key end-use markets for R-PO include automotive, construction, bin bags, outdoor furniture and packaging. Automotive demand has already fallen sharply because of the outbreak, and it is likely to decline further after temporary closures at automotive manufacturers across Europe.

The construction industry is more protected from any direct production impact caused by the coronavirus, but is likely to be heavily affected by any economic downturn. Outdoor furniture demand, meanwhile, is also likely to suffer due to isolation measures.

In contrast, packaging demand is expected to soar. Buyers are expected to favor plastic-wrapped food driven by hygiene concerns, and because of the widespread use of polyolefins in packaging cleaning and hygiene products.

Concerns

Nevertheless, the extent to which this will benefit the recycling industry remains unclear. Several sources suggest that the pandemic will take the focus off sustainability targets in the short term. They also expect brand owners to switch back to virgin, which may be more readily available.

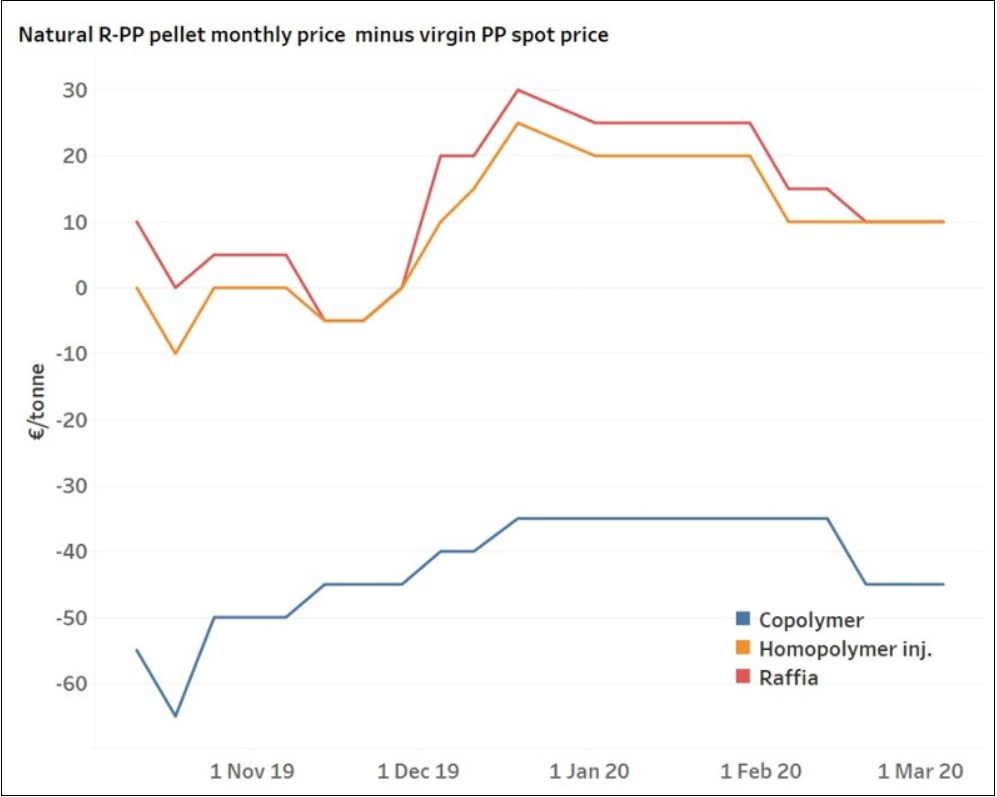

Because the price for products such as colorless R-PET flakes and food-grade pellets, high density polyethylene (R-HDPE) natural and food-grade pellets and R-PP natural pellets are all now higher than virgin material, it only adds to the possibility of further substitution back to virgin.

“In the current situation, if they can't find recycled low-density polyethylene (R-LDPE) they'll use LDPE simply to [be able to] supply [their goods],” a major packaging manufacturer said.

Coupled with this, there are concerns about staff shortages as the pandemic gathers pace, and the ability of smaller recyclers to manage cash flow if they are unable to operate for a sustained period of time. Cash reserves at recyclers are typically kept low compared with the petrochemicals industry.

Of wider concern is the impact on logistics. Now that several countries across Europe have closed their borders (see map below) and restricted the movement of goods and people, getting material to and from recycling units is already proving a challenge for some.

“We see [problems] on the logistics side, so getting bottles delivered, and also delivery of our finished goods. There are some borders closed but it's mainly focused on people trends, not transport of goods... Checks on temperatures [of drivers] at borders… delay transport activities,” an R-PET producer said.

Across the recycling industry, pan-European trade flows are common with both post-consumer and post-industrial waste commonly sourced from overseas—depending on availability and quality—and finished recycled flakes and pellets also commonly exported cross-border.

“Logistics is very painful at the moment in Europe, for all products and all materials, don't know what it'll mean in the end as it'll impact the usage of the products,” a flake producer in central Europe said.

Logistic problems are already causing some companies to build up inventories to manage any potential disruption.

“We buy big quantities from France, Netherlands and Italy and when the borders close completely there's a big problem as where do we get our material? Also 50% [of our end product] goes outside of Germany to Europe and our customers ask us if we're able to deliver the material they need, if we have to reduce production.

“When we ask our plants for transport, they say no problem. At the moment it seems to be… stable, but the question is what will happen tomorrow when the government makes the decision to close the border,” a major European recycler said.

Ongoing uncertainty over the wide array of response by European governments to the coronavirus has further obscured the demand picture—while some are stockpiling, others are taking the opposite approach and avoiding new orders.

“We have orders, but not new orders for the next weeks. There's a big confusion over the next weeks,” the major French waste collector and reprocessor said.

The longer-term impact on investment decisions also remains uncertain. Investment across both mechanical and chemical recycling is vital if the industry is to meet ambitious legislative and brand targets for packaging recycling. There is a current severe shortage of food-grade material across all recycled polymers—both on the collection and reprocessing side.

Take R-PET as an example. Reprocessing capacity for food-grade approved pellets stands at 300,000 tons/year, whereas for recycled R-HDPE it is around 100,000 tons/year.

For other R-PO grades, food-grade material is only available in very small volumes because of European Food Safety Authority (EFSA) requirements on traceability and sorting.

New technology, new collection methods, the growth of chemical recycling and increased reprocessing capacity are all needed to meet 2025 targets.

However, a weaker economic outlook is having a limiting effect on investment, particularly in areas such as recycling where investment from small start-ups is common due to lower barriers to entry than for petrochemicals, and where collection systems remain largely in the control of local authorities. Both are vulnerable in the current situation,

The economic fallout from the global recession of 2008, for example, resulted in more than a decade of underinvestment in collection systems by local authorities because of widespread austerity measures across Europe.

With the scale of social distancing measures necessary for the containment of the pandemic, a global recession is looking increasingly likely.

For the time being, the majority of the European recycling industry continues to operate on a business as usual basis - but the consequences may be felt for many years to come.

Coupled with this, there are concerns about staff shortages as the pandemic gathers pace, and the ability of smaller recyclers to manage cash flow if they are unable to operate for a sustained period of time. Cash reserves at recyclers are typically kept low compared with the petrochemicals industry.

Of wider concern is the impact on logistics. Now that several countries across Europe have closed their borders (see map below) and restricted the movement of goods and people, getting material to and from recycling units is already proving a challenge for some.

“We see [problems] on the logistics side, so getting bottles delivered, and also delivery of our finished goods. There are some borders closed but it's mainly focused on people trends, not transport of goods... Checks on temperatures [of drivers] at borders… delay transport activities,” an R-PET producer said.

Across the recycling industry, pan-European trade flows are common with both post-consumer and post-industrial waste commonly sourced from overseas—depending on availability and quality—and finished recycled flakes and pellets also commonly exported cross-border.

“Logistics is very painful at the moment in Europe, for all products and all materials, don't know what it'll mean in the end as it'll impact the usage of the products,” a flake producer in central Europe said.

Logistic problems are already causing some companies to build up inventories to manage any potential disruption.

“We buy big quantities from France, Netherlands and Italy and when the borders close completely there's a big problem as where do we get our material? Also 50% [of our end product] goes outside of Germany to Europe and our customers ask us if we're able to deliver the material they need, if we have to reduce production.

“When we ask our plants for transport, they say no problem. At the moment it seems to be… stable, but the question is what will happen tomorrow when the government makes the decision to close the border,” a major European recycler said.

Ongoing uncertainty over the wide array of response by European governments to the coronavirus has further obscured the demand picture—while some are stockpiling, others are taking the opposite approach and avoiding new orders.

“We have orders, but not new orders for the next weeks. There's a big confusion over the next weeks,” the major French waste collector and reprocessor said.

The longer-term impact on investment decisions also remains uncertain. Investment across both mechanical and chemical recycling is vital if the industry is to meet ambitious legislative and brand targets for packaging recycling. There is a current severe shortage of food-grade material across all recycled polymers—both on the collection and reprocessing side.

Take R-PET as an example. Reprocessing capacity for food-grade approved pellets stands at 300,000 tons/year, whereas for recycled R-HDPE it is around 100,000 tons/year.

For other R-PO grades, food-grade material is only available in very small volumes because of European Food Safety Authority (EFSA) requirements on traceability and sorting.

New technology, new collection methods, the growth of chemical recycling and increased reprocessing capacity are all needed to meet 2025 targets.

However, a weaker economic outlook is having a limiting effect on investment, particularly in areas such as recycling where investment from small start-ups is common due to lower barriers to entry than for petrochemicals, and where collection systems remain largely in the control of local authorities. Both are vulnerable in the current situation,

The economic fallout from the global recession of 2008, for example, resulted in more than a decade of underinvestment in collection systems by local authorities because of widespread austerity measures across Europe.

With the scale of social distancing measures necessary for the containment of the pandemic, a global recession is looking increasingly likely.

For the time being, the majority of the European recycling industry continues to operate on a business as usual basis - but the consequences may be felt for many years to come.

LinkedIn